There's a loan officer out there right now doing $100M in volume. He's working 60 hours a week, managing a call center, spending $150,000-$300,000 a month on rate table leads, and pocketing 11 basis points on every deal.

And there's another loan officer doing $30M a year, working normal hours, with a tight team and a dialed-in system -- making 111 basis points a unit and taking home more money.

The first guy thinks the second guy isn't ambitious enough. The second guy thinks the first guy is one bad quarter away from disaster.

He's right.

Quick Answers

Why do rate-focused loan officers struggle to build profitable businesses?

Rate competition attracts low-loyalty borrowers, compresses margins to 10-20 basis points, and creates dependency on expensive paid leads. When rates shift or lead platform costs increase, there's no buffer. The business has no retained client value -- every deal starts from zero.

What do top-producing loan officers focus on instead of rate?

Top producers stay genuinely useful to past clients and referral partners between transactions -- sharing relevant market insight, flagging real opportunities, giving advice that has nothing to do with closing a deal. They earn the right to be top-of-mind. Their pipelines compound because every closed loan creates a future referral or repeat transaction -- not because they sent an automated birthday email.

What is the execution gap in mortgage?

The execution gap is the distance between what loan officers know they should be doing (staying in front of past clients, maintaining referral relationships) and what they actually do consistently without a system forcing it. Most LOs know what works. Very few do it reliably.

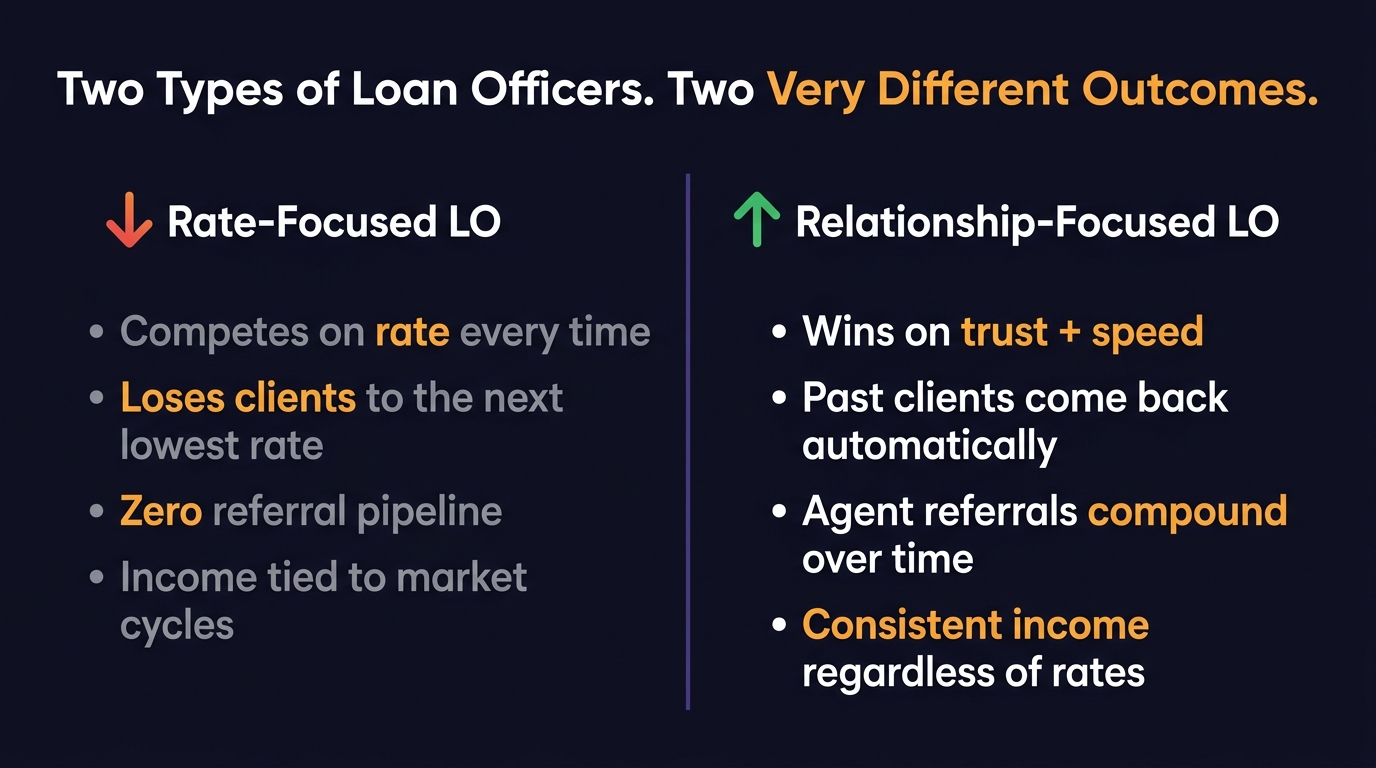

The Rate Table Trap

Competing on rate feels like a volume play. Lower your margin, capture more leads, close more deals. The math seems to work -- until it doesn't.

The problem isn't just margin compression. It's structural.

You attract the least loyal borrowers. A rate-shopper who chose you because you were 0.125% lower will leave you the same way. There's no relationship, no referral, and no database value when it's over.

Your cost to acquire a customer is always going up. Lead platforms know exactly what rate-focused LOs will pay. They price accordingly. As more LOs chase the same leads, acquisition cost climbs and margin shrinks.

You're building a business that depends on volume you can't control. Rate table leads are directly tied to rate environments. When rates move against you, your pipeline moves with them -- but your overhead doesn't.

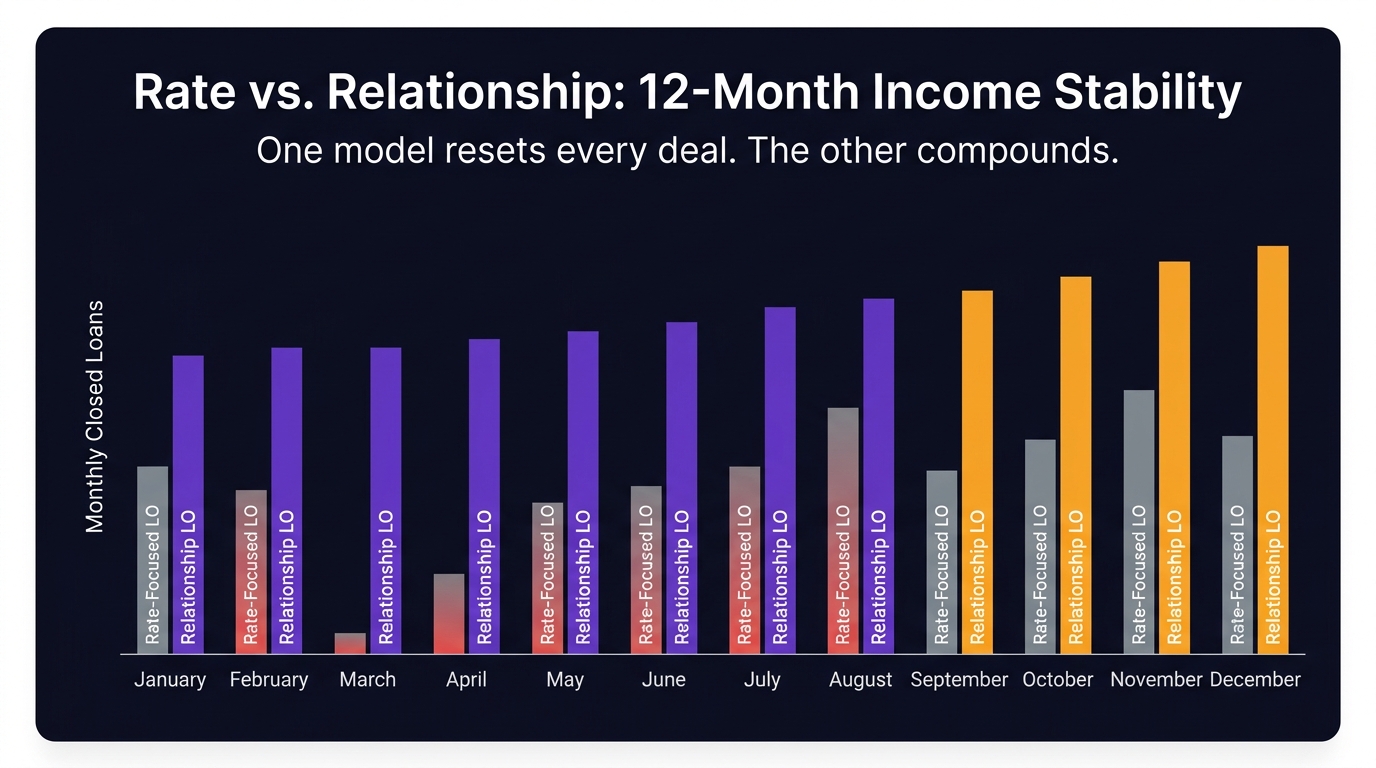

What the Numbers Actually Show

At a recent industry conference, LOs were asked to share their volume and net income. The pattern was consistent: the highest-volume shops running rate table economics reported the lowest net income. The outliers doing comparable or higher net -- with a fraction of the volume -- were universally running referral-first, relationship-based models.

The math is simple:

- 100 loans at 11 bps average = thin net, high overhead, high churn

- 40 loans at 111 bps average = higher net, manageable overhead, compounding database

The rate-table operator has to keep pushing to refill a pipeline that resets to zero after every close. The relationship operator has a pipeline that pulls.

The Execution Gap

Here's where most LOs get this wrong: they think the shift from rate-focused to relationship-focused is a mindset problem. It's not. It's about execution.

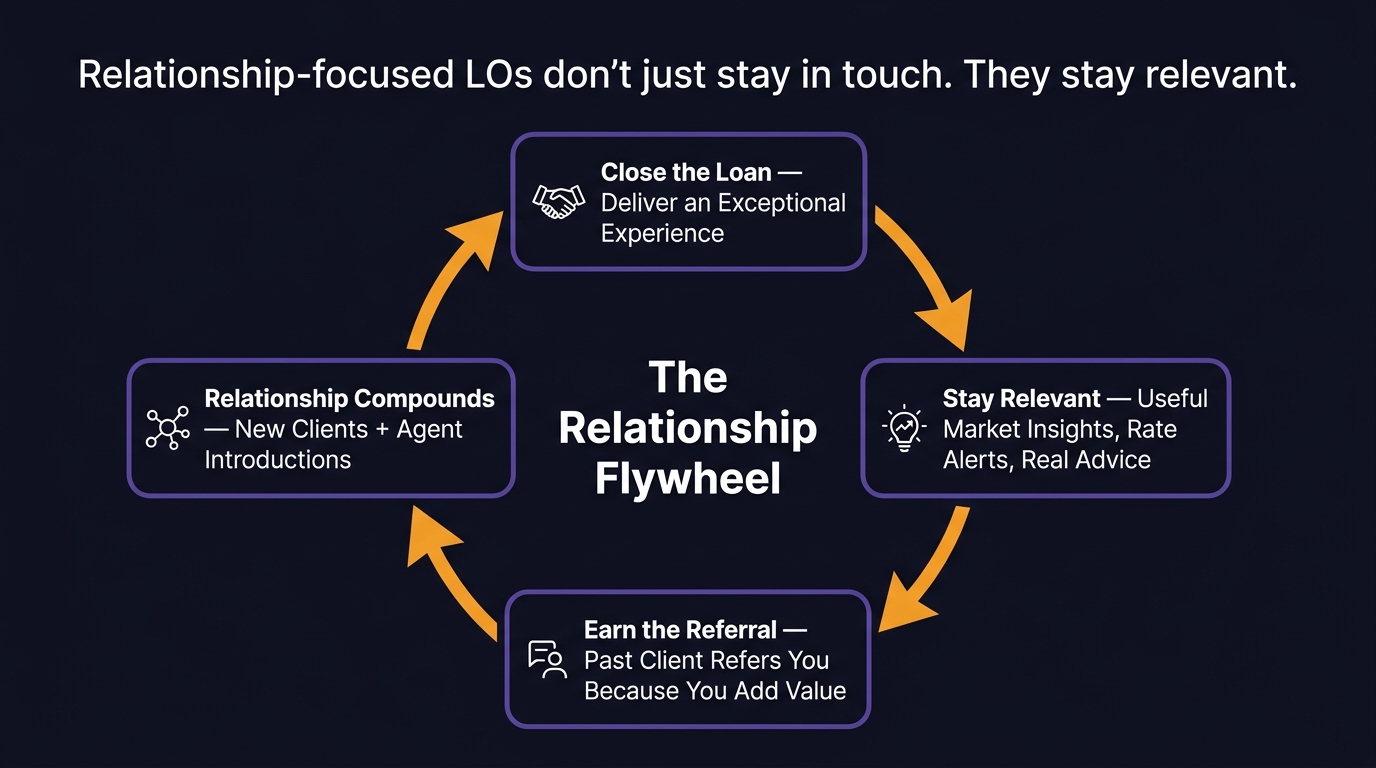

The relationship-first model only works if you actually stay relevant. Not "touching base" every 90 days. Relevant -- meaning you show up with something worth their time. A rate alert when it genuinely makes sense for that specific borrower to refinance. A market update when their neighborhood is moving. A referral recommendation because you actually know someone. Real value, not noise.

The systems problem is this: delivering that kind of value consistently to hundreds of past clients and referral partners is impossible to do manually. The LOs who pull it off aren't doing more work -- they have infrastructure that surfaces the right action at the right time. Technology handles the consistency and the timing. The LO handles the relationship.

What Top Producers Actually Do

1. They treat their database like a business asset -- and they stay useful to it.

Every closed loan is a potential refinance, a referral, or both. But that only converts if the borrower still trusts you and thinks of you first. An LO with 200 closed loans who has been consistently relevant to those clients -- sharing things they actually found useful -- has meaningful future business in that database. An LO who hasn't been in touch since the closing disclosure has a list.

2. They make referral partner relationships systematic, not random.

The best referral relationships aren't built on coffee meetings or drip campaigns. They're built on being consistently useful -- sharing something that helps that specific agent's business, making introductions, flagging market opportunities before they're obvious. The system's job is to make sure that relevance doesn't fall off when you get busy. The relationship is still yours to earn.

3. They stop chasing cold leads and start reactivating warm ones.

A lead that came in 90 days ago and went quiet isn't a dead lead. It's a lead that didn't get a compelling reason to re-engage. The difference between a dead lead and a reactivated one usually isn't persistence -- it's relevance. Following up with something genuinely useful (a program they qualify for, a rate move that changes their math) converts. Following up with "just checking in" doesn't.

4. They know their numbers.

Response rate on initial follow-up. Conversion rate from application to close. Referral source attribution by partner. The LOs who grow consistently can tell you exactly where their business comes from and what's working. The ones who plateau usually can't.

Key Takeaways

- Rate competition produces volume, not profit. Margin compression and high lead costs make it structurally unsustainable.

- Top producers compete on relevance, not rate. Their pipeline compounds because every deal creates future value -- if they've earned the right to stay in touch.

- The gap between knowing this and doing it is a systems gap, not a mindset gap. The right technology makes the relationship-first model executable at scale.

- Past clients and referral partners are your highest-ROI lead sources. They're also the ones most LOs are underinvesting in.

Frequently Asked Questions

Can a loan officer compete without offering the lowest rate?

Yes -- and the data consistently shows that relationship-focused loan officers out-earn their rate-focused counterparts at lower volume. Borrowers who choose their LO based on trust and service are more likely to close, more likely to refer, and more likely to come back.

What's the best lead source for mortgage loan officers?

Past clients and real estate agent referrals consistently produce the highest conversion rates and lowest cost per funded loan. Paid lead sources like rate tables have their place in a diversified strategy but should not be the primary pipeline driver.

How do top loan officers stay relevant to past clients between transactions?

The ones who do it well aren't sending generic check-in emails -- they're delivering things that are actually worth opening: rate movement that affects that specific borrower's situation, local market updates that matter to a homeowner in that neighborhood, a referral or resource relevant to where they are in life. Technology makes it scalable. The LO still has to make sure what's being delivered is actually worth something.

The Bottom Line

Rate competition is a race to the bottom. You can win at it technically -- but winning means high volume at very little margin with no cushion when the market shifts.

The loan officers building durable, profitable businesses aren't competing on rate. They're competing on relevance, trust, and consistency. They're harder to displace, more profitable per deal, and less exposed to rate environment risk.

The tools exist to build that kind of business. The question is whether you're using them.