If you search for "mortgage marketing ideas" right now, you are going to find the same generic, recycled advice from 2018.

The internet is full of "gurus" telling loan officers to post three TikToks a day, buy shared Zillow leads, and drop off donuts at real estate offices. It is a formula designed to keep you busy, not profitable.

The reality of mortgage marketing in 2026 is simple: you do not need more clever ideas. You need a system that captures high-intent borrowers and works your past database relentlessly. Let's break down exactly why the old ways are dying, and what the top 1% of producers are doing to scale their pipelines in a tight market.

1. Stop Buying Garbage Leads (The Reality Check)

The default strategy for most loan officers is to buy internet leads from massive aggregators like LendingTree or Zillow. It feels like action, but it's usually just throwing money into a black hole.

Here is the problem with that model: you are buying shared data. The moment that lead hits your inbox, it has also been sold to five other loan officers. You are instantly forced into a race to the bottom on price and speed. Unless you are running a massive call center floor with automated dialing systems and an offshore ISA team, you are going to lose that fight.

The Conversion Reality

Industry data shows that shared internet leads convert at less than 1.5%. You are paying to be the 4th person to call an annoyed prospect. A sustainable mortgage business cannot be built on low-intent, shared data. You need exclusive leads who are actually looking for you.

2. The Database Reactivation Goldmine

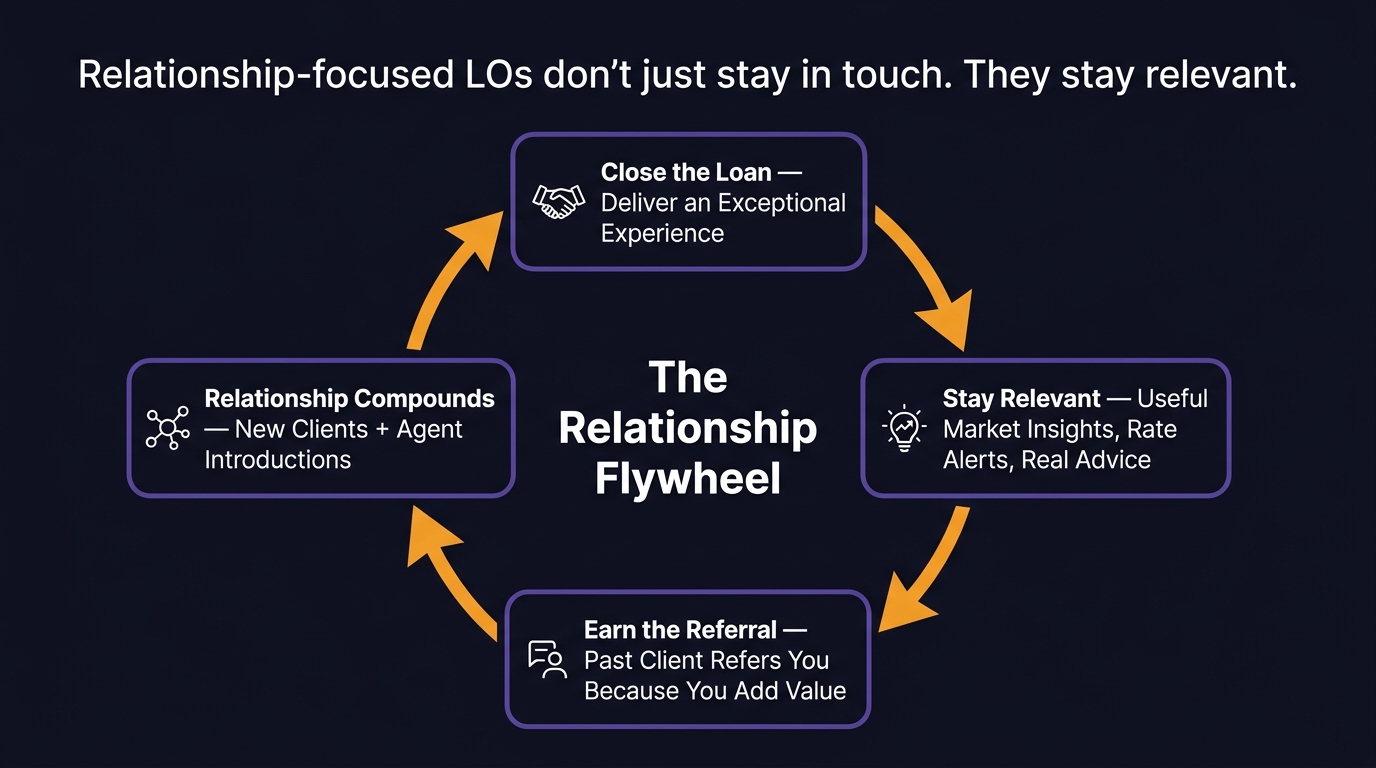

Before you spend a single dollar on new advertising, you have to fix your leaky bucket. Most loan officers sit on a database of hundreds of past clients and completely ignore them until they decide it is time to send a generic holiday card. This is where millions of dollars in origination volume is lost every single year.

Your past client database is your single highest-ROI asset. The anti-guru plan starts with aggressive, automated database reactivation.

This means setting up systems to monitor your past clients for opportunities. If a past client's home equity spikes, or if current rates drop below their locked rate, your system should automatically trigger a personalized email and SMS alert.

You do not need to manually check rates every morning. Tools like the Empower Toolkit allow you to set up automated rate drop alerts, equity updates, and highly-relevant newsletters so you stay top-of-mind. When they are ready to refinance or buy an investment property, they call you first. This transforms your database from a static spreadsheet into an active lead generation machine.

3. The High-Intent Playbook: Why Google Ads Crush Facebook Ads

When loan officers finally decide to run their own ads, they almost always default to Facebook. They run ads for listing photos or generic homebuyer seminars.

Facebook is interruption marketing. People are on Facebook to look at photos of their friends, not to shop for a mortgage. The intent is incredibly low, which means you have to constantly churn through new videos, new images, and new ad copy just to keep people clicking. You are catching people at the top of the funnel, months before they actually need a loan.

If you want to get mortgage leads that actually convert, you need search marketing. You need Google Ads.

When someone searches "best mortgage lenders near me" or "current FHA rates in Texas" on Google, they are actively hunting for a solution. They have their wallet in hand. They aren't browsing; they are deciding.

Facebook Ads

- Low intent (interruption)

- Constant creative fatigue

- Longer incubation periods

- Higher volume, lower quality

Google Search Ads

- High intent (solution seeking)

- Set-and-forget text ads

- Shorter sales cycle

- Lower volume, higher closing ratio

While the cost per lead (CPL) on Google is similar to Facebook, the intent is exponentially higher. Plus, Google Search Ads require significantly less creative upkeep over time. You do not need to shoot new videos every week; you just need tightly optimized search text and a landing page that converts.

4. The "Trojan Horse" Realtor Strategy

The hardest part of being a loan officer is convincing real estate agents to send you their buyers. Dropping off coffee, buying donuts, and dropping off rate sheets does not work anymore. It positions you as a subordinate vendor begging for crumbs.

Instead of begging for business, bring business to them.

Using Google Ads, you can set up a co-marketing campaign with a top-producing realtor. You split the cost of the ad spend. You target high-intent homebuyers searching for properties in their zip code. The realtor gets the buyer lead, and you get the pre-approval.

This positions you as a strategic partner who actually drives revenue, rather than just another vendor asking for a handout. When you control the lead flow, you control the relationship.

The Execution System

The reason most loan officers fail at this plan is the "Execution Gap." They know they need to run Google Ads, reactivate their database, and build landing pages, but they try to duct-tape five different software platforms together to do it. The complexity kills the execution.

You do not need to become a digital marketer or a Zapier expert to execute this plan.

Empower LO provides the complete system. The Empower Toolkit gives you the CRM, the funnel builder, and the automated database reactivation campaigns all in one place. And with our LeadEngine service, our team fully manages your high-intent Google Ads campaigns for you.

Stop buying shared leads and wasting time on Facebook. Build an execution system that actually generates exclusive, high-intent deals.